Disclaimer: Unless otherwise stated any opinions expressed below belong solely to the author, who doesn’t hold any stake in Sea Ltd. or any of its competitors.

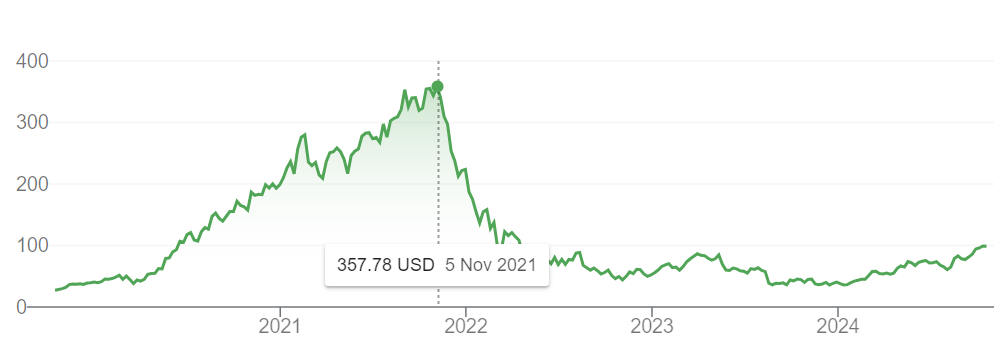

Following the implosion of the inflated tech stocks in late 2021 Sea Ltd. lost around 90 per cent in value at its lowest point, as money hastily receded. Now, however, the one time darling of the investors is gradually clawing back its position.

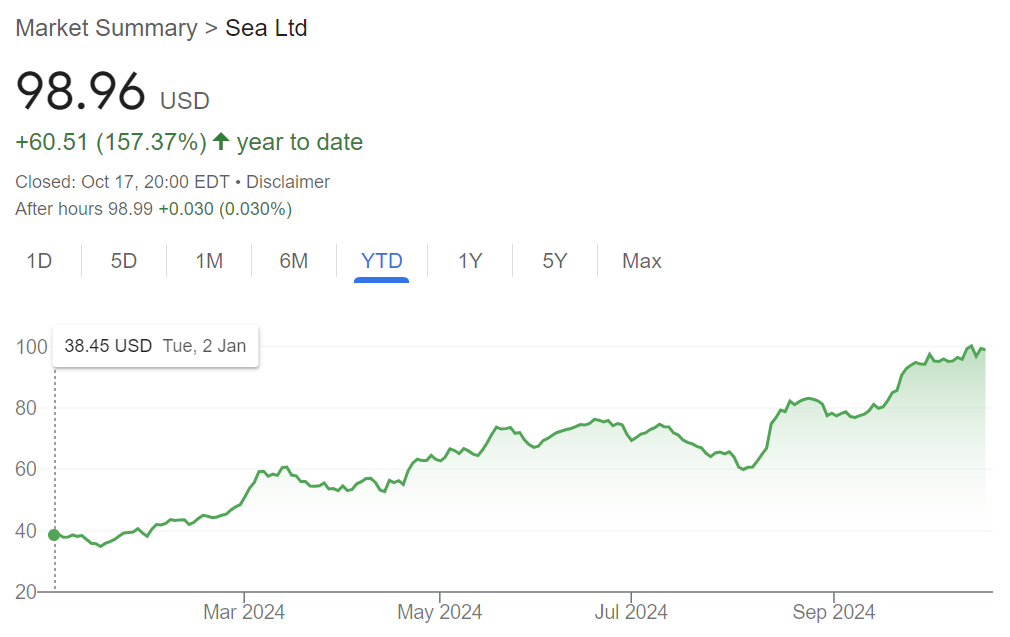

The stock is once again trading at close to US$100 per share—perhaps a far cry from the $350 it hit three years ago, but certainly a lot more respectable than the mid-30s it saw last year. Yes, if you invested in Sea last August you would have nearly tripled your money by now, after the stock gained over 170 per cent (over 150 this year alone).

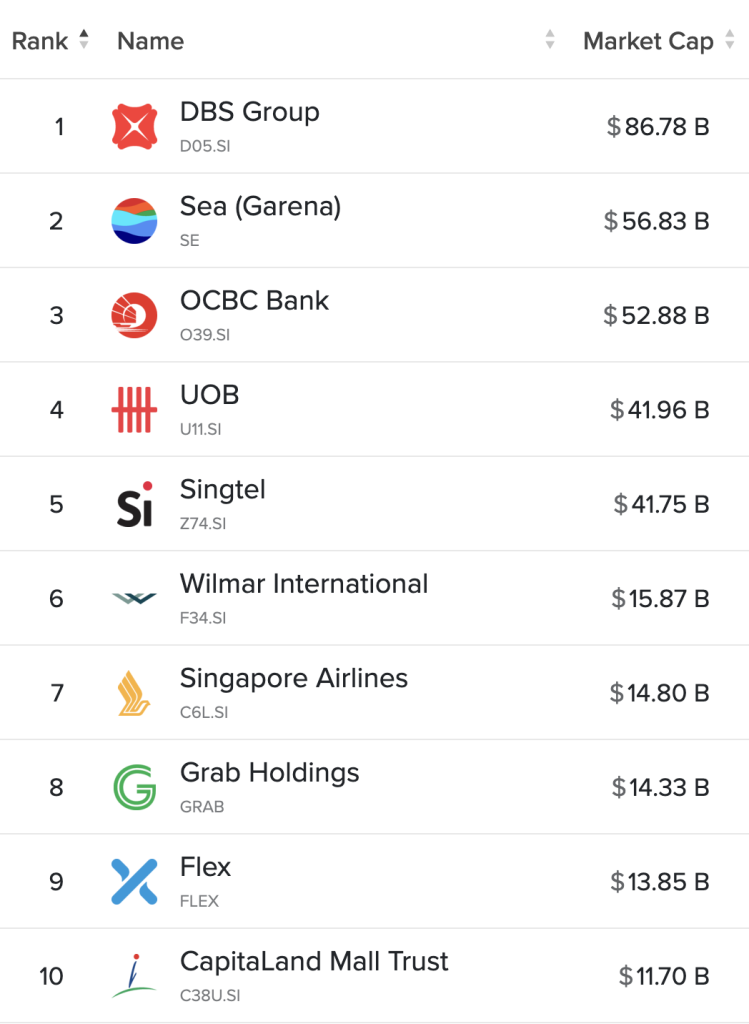

Its 2024 rally added more than US$34 billion to its value, putting its market capitalisation above US$56 billion, more than OCBC’s US$52 billion and second in Singapore only to DBS:

Why is Sea attractive again?

In one word? It matured. We could dissect the quarterly earnings reports to seek guidance in figures going up or down, but in reality it’s about the bigger picture.

The last time Sea was red hot it was not only on the back of a huge surge in capital flooding stock markets back in 2021, on the back of a Covid rebound fueled by government stimulation of the economy in the USA, but it was one of those hyper-growth startups which bode well for the future.

It didn’t make any money but it grew rapidly and expanded to new markets.

But once the bull market turned into a collapse, as investors realised their gains and turned more cautious as tech industry in general saw huge drops in value, Sea had little to prop it up.

What’s worse, the post-Covid thawing of lockdowns meant that people neither spent as much time gaming online as before (hurting Garena) nor shopping (what slowed Shopee’s rapid growth).

Add to that the fact that Sea wasn’t turning a profit and the cash reserves it had built up could last for two to three years of its high burn rate, the prospects weren’t very good, including a non-trivial risk of bankruptcy, given that raising capital was no longer cheap.

The subsequent two years had been spent on addressing the fundamentals, cutting costs and pushing the company into the black—which it, amazingly, achieved already in Q4 of 2022.

However, concerns grew again, this time over growth.

After all, investors are not looking for dividend payouts from a company that barely breaks even. They seek high return on investment in the form of stock appreciation, which depends on its growth.

But growth had slowed down and Forrest Li had to abandon prudence and spend more again to support revenue in the middle of 2023, what put Sea back in the red and sent the stock tumbling again, from over $80 in May to just $36 in August of that year.

Today, however, it seems that investors have grown comfortable that the company is, a) able to survive, so their downside risk has been significantly reduced, and b) presents attractive prospects, increasing its results by healthy two digits year on year.

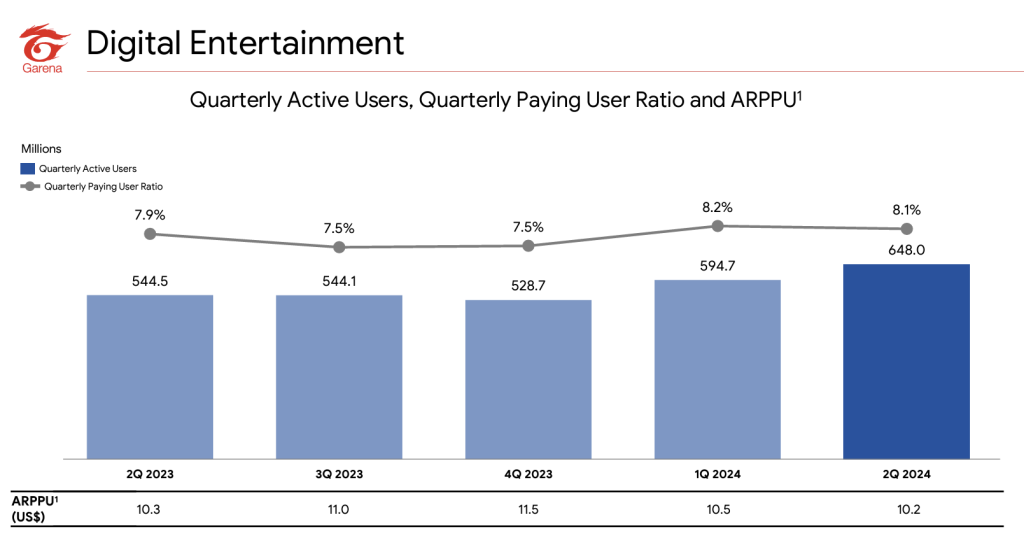

As of last quarter all of its business units are growing, including Garena, which suffered a painful post-Covid slip that it has now rebounded from.

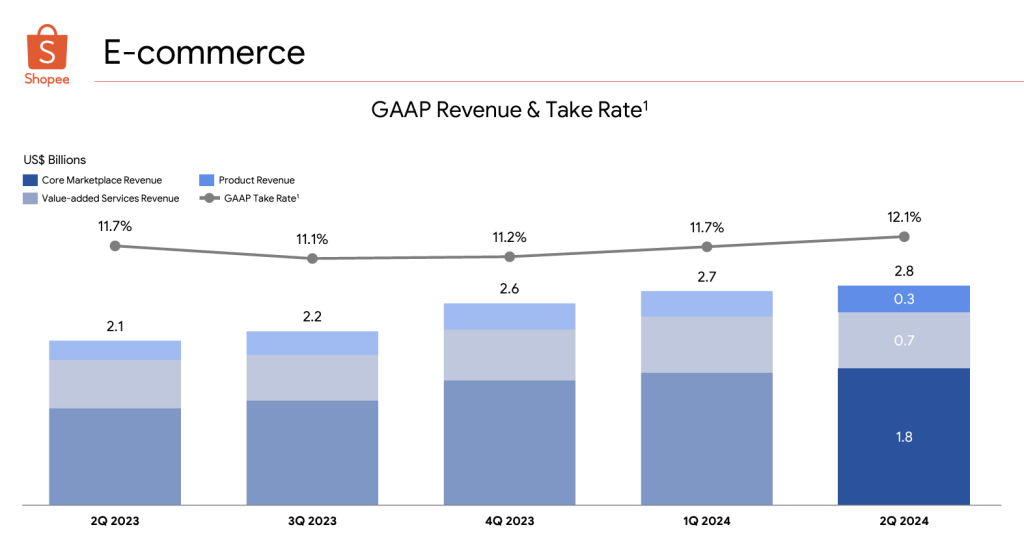

Shopee maintains its trajectory, seeing its revenue increase by $700 million year on year—or by one third—while bumping its take rate, which is expected to further increase as Sea hiked its commissions recently.

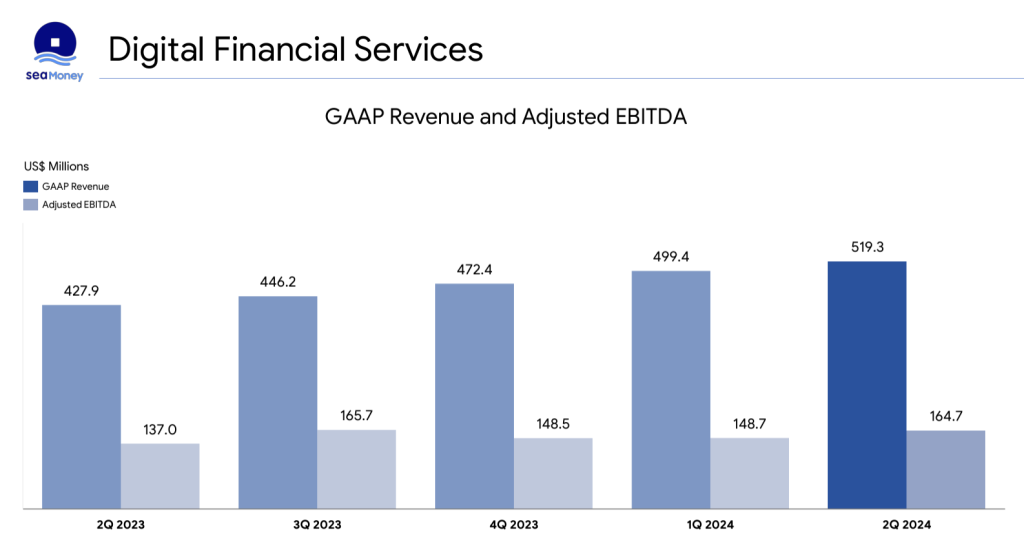

Finally, SeaMoney, the digital finance arm of the business holds its upward course as well, generating over half a billion in quarterly revenue already.

Moreover, Sea didn’t have to dip into its cash reserves too deep even in the most demanding of times, meaning that it still holds onto US$9 billion, giving it a healthy margin for adjustments and investments on a needs basis.

The spectre of bankruptcy appears to have been extinguished and the company is here to stay, while still capable of producing high growth amid less than ideal conditions.

It’s a mature business now and is treated as such.

Featured Image Credit: Sea