")

At the point of update, there are 650 stocks listed on the Singapore exchange. I’ve limited the dataset to the Straits Times Index (STI) constituent stocks, then use the SGX Stock Screener to filter for those with a Price-to-Book (PB) ratio of less than 1 which means that they are trading below their net asset value.

Would we be able to find undervalued blue chip stocks in the Singapore market today? Well as of 1 Dec 2023, here are the 8 undervalued stocks in Singapore we’ve identified.

Will these 8 undervalued blue chip stocks help you huat? Let’s find out:

8 undervalued stocks in Singapore (Dec 2023)

| Stock | Ticker | Market Cap ($, B) | Price / Book | P/E Ratio | Dividend Yield | Industry |

|---|---|---|---|---|---|---|

| Frasers Logistics & Commercial Trust | BUOU | 3,107 | 0.91 | 6.3% | Industrial REITs | |

| Seatrium Limited | S51 | 5,355 | 0.88 | 0.0% | Machinery | |

| Wilmar International Limited | F34 | 16,942 | 0.87 | 9.51 | 4.7% | Food Products |

| Mapletree Pan Asia Commercial Trust | N2IU | 5,377 | 0.76 | 20.20 | 6.6% | Retail REITs |

| City Developments Limited | C09 | 4,244 | 0.64 | 25.62 | 3.2% | Real Estate Management & Development |

| UOL Group Limited | U14 | 3,727 | 0.47 | 19.42 | 2.5% | Real Estate Management & Development |

| Jardine Matheson Holdings Limited | J36 | 11,189 | 0.39 | 22.60 | 5.7% | Industrial Conglomerates |

| Hongkong Land Holdings Limited | H78 | 7,105 | 0.22 | 6.8% | Real Estate Management & Development |

8. Frasers Logistics & Commercial Trust (BUOU): P/B 0.91

Frasers Logistics & Commercial Trust (FLCT) is a REIT that gives you exposure to a portfolio of 105 industrial and commercial properties valued at ~S$6.5 billion across five major developed markets.

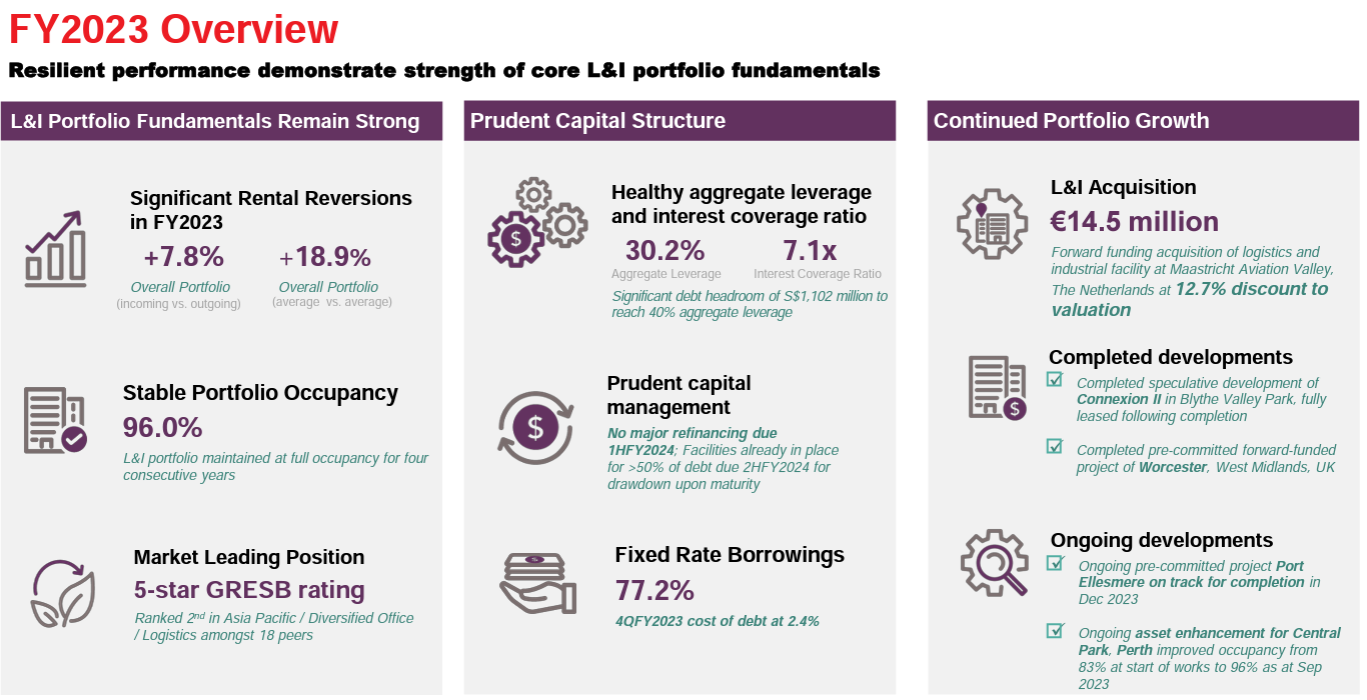

As of FLCT’s latest business update, they have maintained a healthy aggregate leverage at 30.2% and 77.2% of their borrowings were made at fixed rates.

FLCT had reported a FY23 DPU of 7.04 cents, which is down 7.6% from FY22. It is currently trading at a P/B of 0.91. Compared to its historical P/B of 1.3 and their industry sector’s P/B of 0.8, FLCT appears to be slightly undervalued. That said, Singapore REITs have taken a hit lately due to the poor macroeconomic situation, and the headwinds will continue to haunt REITs.

If you’re a REIT investor, here’s what you must know about the state of S-REITs now.

7. Seatrium (S51): P/B 0.88

After Sembcorp Marine merged with Keppel Offshore & Marine (Keppel O&M), it announced a rename to “Seatrium” on 27 April 2023, to better reflect its business and aspiration to be a premier global player.

While Keppel Corporation investors rejoiced at the spin off of the floundering O&M arm, Sembcorp Marine investors had little to celebrate. After all, both Sembcorp Marine and Keppel O&M were struggling due to the downturn in the offshore and marine sector.

It is still too early to determine if Seatrium will be able to recover to previous highs. The company had announced on 8 November that losses are expected for FY2023, despite having grown its net order book to S$17.8billion so far.

Seatrium is now trading at about -89% off its 5 year high. Given that the O&M industry is cyclical, Seatrium is well positioned to recover during the next cycle. But, “when will the next cycle come?” remains a question that only the gods can answer.

Seatrium is currently trading at a P/B of 0.88, which is lower than its historical P/B of 1, making it slightly undervalued.

6. Wilmar International Limited (F34): P/B 0.87

Wilmar International is a consumer goods and commodity conglomerate involved in the entire supply chain. Some of its business processes include the cultivation of palm oil and sugarcane, distribution of consumer food products as well as processing and distribution of animal feeds and industrial agri-products like biodiesel.

Wilmar has been paying dividends since 2013 and has an average 5 year dividend yield of 3.7%. Wilmar paid a dividend of SGD0.11 per share in May 2023 and at the point of writing, its dividend yield is about 4.6%.

At the current update, Wilmar International is currently trading at a P/B of 0.87, which is lower than its historical P/B of 1.

5. Mapletree Pan Asia Commercial Trust (N2IU): P/B 0.76

Mapletree Pan Asia Commercial Trust (MPACT) is the renamed entity after Mapletree Commercial Trust (MCT) acquired and merged with Mapletree North Asia Commercial Trust on 3 Aug 2022. Following the merger, MPACT now has 18 properties across five key gateway markets of Asia – five in Singapore, one in Hong Kong, two in China, nine in Japan and one in South Korea. We covered the merger here.

While MPACT is currently undervalued (based on its Price/book), it has delivered outstanding results over the last 10 years. Alvin shares his latest deep dive into SREIT performance here.

Although its Singapore portfolio did well, MPACT’s performance is being held back by the rest of its North Asia portfolio and this trend will likely continue for the near future. You’ll need to be comfortable knowing that markets like China and Hong Kong may not perform as well, especially in the short term.

The REIT has also taken measures to defend against headwinds. It has increased its fixed rate debt from 72.5% in 2022 to the current 79.9%. However, its Aggregate Leverage Ratio remains at 40.7% and adjusted Interest Coverage Ratio has lowered to 3x (from 4.4x last year).

On the dividend yield front, MPACT is currently yielding 6.6% (at the point of writing):

As of the current update, MPACT is currently trading at a P/B of 0.76. Compared to its historical P/B of 1.3, MPACT seems to be underpriced currently.

4. City Developments (C09): P/B 0.64

City Developments Limited (CDL) is a real estate operating company with a diverse property portfolio of residential, commercial and hotel properties (M social and Millennium hotel brands) located worldwide. They are involved in property development, asset management and hotel operations. CDL also owns ~ 50% of iREIT Global which has a portfolio of commercial and retail properties across Europe.

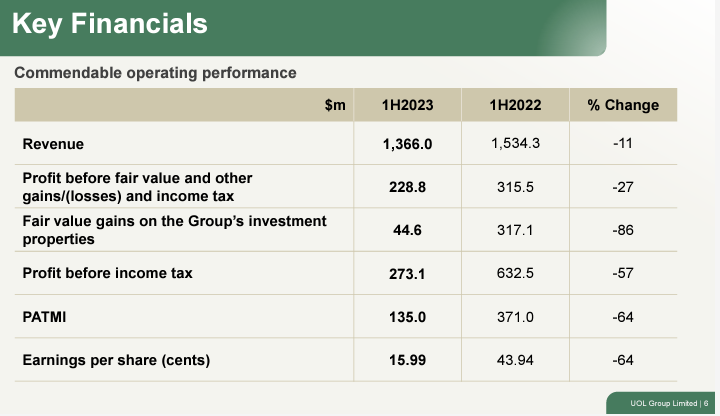

As of 1H23, CDL has recorded an 80% increase in revenue against previous year’s performance and continues to have several developments and acquisitions in its pipeline. At the same time, CDL has increased its Fixed Rate Debt to 46% (from 42% in the previous year), although its net gearing has also gone up from 51% previously to the current 57%.

As of the current update, City Dev is currently trading at a P/B of 0.64. Compared to its historical P/B of 0.8 and their industry sector’s P/B of 0.8, City Dev seems to be undervalued. CDL had also announced a dividend of $0.04 for 1H23 (vs $0.12 in 1H22).

3. UOL (U14): P/B 0.47

UOL is a real estate management company with an extensive portfolio of development and investment properties.

Business hasn’t been smooth for UOL. It had reported a -11% in revenue, -27% in profits and -64% in EPS. Its property development arm was the key segment that was holding its revenue down which could be due to the lower number of projects in the preceding years.

At the point of update, UOL’s dividend yield is about 2.5%. Historically, UOL’s dividend yield was as such:

Its current P/B of 0.47 is lower than its historical P/B of 0.7.

2. Jardine Matheson Holdings (J36): P/B 0.39

Jardine Matheson (JDM) is a conglomerate with a diverse range of businesses under its umbrella, with a hand in sectors ranging from property to retail and even heavy machinery and construction.

Given JDM’s complex business and size, Alvin had ranked it as “JOMO” in his Singapore Blue Chip Stocks ranking video.

It holds 75% of Jardine C&C, 52% of Hongkong Land and many more.

JDM has continued paying out dividends through the dark pandemic years and at the point of update, its dividend yield is ~4.4% for the full financial year of 2022.

Jardine Matheson is trading at a P/B of 0.39 at the point of update which is below its historical P/B of 0.7 and its industry average of 0.9 which suggests that it might be undervalued. You should note that JMD’s business can be rather cyclical.

1. Hongkong Land (H78): P/B 0.22

Hongkong Land is a property investment, development and management group and is considered one of the property blue chip stocks in Singapore.

As its name suggests, most of its portfolio is concentrated in Hong Kong (57%). In Singapore, Hongkong Land owns part of the Marina Bay Financial Centre (MBFC) properties. Their portfolio of investment properties are primarily office and retail properties, and recently made our list of Singapore Blue Chip stocks with Moats.

However, Hongkong Land continues to struggle due to its exposure to Hong Kong and China properties. Hong Kong’s investment properties are still struggling to recover while the China property market debt crisis has yet to be resolved.

Through it all, Hongkong Land has been actively carrying out its $500 million share buyback programme since Sep 2021. However, that alone may not be sufficient to keep its share price afloat amidst negative macro events such as China’ property market debt crisis and a generally weak Hong Kong property market.

For a deeper analysis on their business model, read Alex’s report here.

That said, Hongkong Land has continued to pay out dividends even through the tough times. At the point of update, its dividend yield is about 6.8% currently.

Hongkong Land’s P/B is currently at 0.22, making it the most undervalued stock on this list. This is also lower than its historical average of 0.3 and its industry P/B of 0.4.

Conclusion

I’ve listed 8 undervalued stocks in Singapore for December, based on their Price-to-Book ratio and I hope this article gave you some investing ideas to research into.

Also, please keep in mind that although PB may be a good primary filter of undervalued stocks, you should do your own deeper research into the fundamentals and performance of any stock that you wish to invest in.

If you’re not sure how to start, refer to our value investing guide, or join Alvin at his upcoming webinar where you’ll learn how you can pick undervalued stocks using Dr Wealth’s i3 investing strategy.