Update: As of 18 Dec 2023, Adobe and Figma have abandoned their merger plans, citing obstacles in the regulatory review process as the key reason. Adobe is reportedly developing a new product, “Ligma” that highly resembles Figma. Alvin shared his thoughts on the fall through of the merger here.

Adobe reported its third-quarter financial results on September 15th, achieving a record sales of $4.43 billion, representing a 13% year-on-year growth. Though it is Adobe’s third consecutive quarter of less than 15% growth, this was not the most shocking news.

Rather, it was the announcement of the acquisition of Figma that surprised many.

The announced merger would be Adobe’s largest acquisition and probably the riskiest in the eyes of investors, leading to the steepest single-day decline of Adobe’s share price in years.

In this post, we’ll look at the acquisition and why it was so resented.

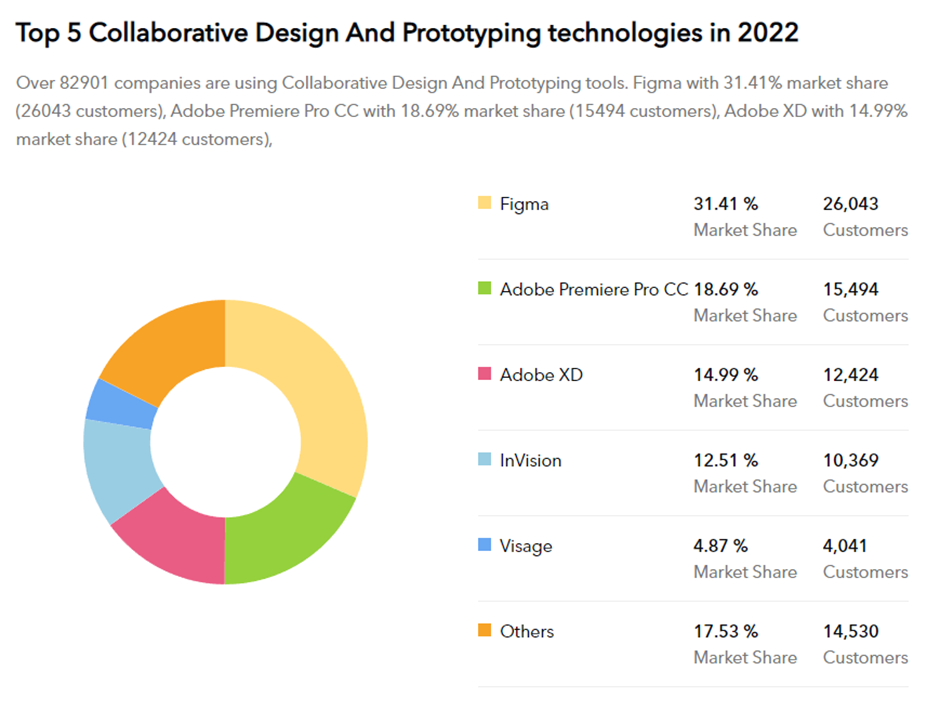

What does Figma do?

Adobe is spending $20 billion to acquire Figma, a leading web-first collaborative design tool.

Figma, which was launched in 2012, was the pioneer of web-based product design. Through multi-player workflows, smart design systems, and a robust, extendable developer ecosystem, it enables anyone who builds interactive mobile and online applications to collaborate.

Figma has garnered millions of designers and developers, as well as a passionate student following, due to the ease of use of its products and a robust developer ecosystem with over a dozen widgets and public plugins.

Along with Canva, another web-based design platform, such waves of browser-based design tools have opened the door for beginners and even non-designers to enter, jeopardising Adobe’s position as the market leader in design software.

Figma currently employs 850 people, and its income is predicted to exceed $400 million in 2022, representing a 100% increase over the previous year.

With a net dollar retention rate of more than 150% and a strong gross margin of 90%, Figma would undoubtedly be labelled as a high-growth SAAS company.

Why did Adobe acquire Figma?

In the eyes of Adobe, there’s synergy between the firms, and having both of these companies together would definitely kill off competition. Given what Figma does, it will undoubtedly take some of Adobe’s users if it continues to grow at its current rate.

Source: slintel

Acquiring competitors would also provide an additional benefit in the form of a stronger moat. With overlapping segments, the merger of Adobe and Figma has the potential to broaden the company’s reach and market opportunities. For example, Figma’s web-based, multi-player capabilities will speed the web distribution of Adobe’s Creative Cloud technologies, making the creative process more productive and accessible to more people to collaborate, thereby increasing Adobe’s reach and addressable market opportunity.

Figma, on the other hand, might benefit from incorporating sophisticated imaging, photography, illustration, video, 3D, and font technology from Adobe.

Overall, the merger will boost top and bottom line growth for both Adobe and Figma through three major drivers:

- Extension of Figma’s reach to Adobe existing customers

- Acceleration of Adobe offerings on the web to next-generation users

- New offerings that is unlocked due to the possibility of collaborative creativity

Sounds good. So why did Adobe’s share price drop drastically?

Acquiring a competitor will undoubtedly enhance Adobe’s moat and eliminate one of its main competitors, but at what cost?

Is Adobe overpaying?

At $20 billion, split about half cash and half stock, this transaction is unquestionably substantial and costly for Adobe. To begin, its sheer scale can be seen by looking at Adobe’s market capitalization. With a market valuation of just under $200 billion before the crash, this transaction represented nearly 10% of the entire firm.

Not to mention how expensive the company is, in terms of value for money. With a $20 billion acquisition cost (twice what Figma was valued in its most recent private funding a year ago) and only $400 million in revenue in 2022, the acquisition is priced at 50x its revenue.

This might have been normal during last year’s tech boom during the pandemic, but with the bearish macro situation we are in this year, most companies have already slipped below 20.

To put things in context, Tesla, a firm many consider to be overvalued, has a Price to Sale (PS) ratio of 15.46. Tesla’s highest PS Ratio for the last 13 years was 30.25.

With Adobe trading at a PS 8.27 and the Figma deal coming in at a PS of 50, we can see why this deal is exorbitant.

Adobe does not have enough cash

Even if you can look beyond its exorbitant valuation, another issue is where will Adobe get the money? Approximately half of the $20 billion will be paid in cash and the other half in shares.

Adobe would have to fork out $10 billion in cash for the deal, which it lacks.

Adobe presently has only $4 billion, so the company would have to find a means to raise the remaining $6 billion. Given that the transaction is only expected to finish in 2023 and that the quarterly profit is roughly $1 billion, some cash could be funneled from there. But its barely enough.

It is highly likely that Adobe would have to finance the deal with a term loan, a move that’s not ideal given rising interest rates.

That said, if the company does so, with an interest coverage ratio of 51.3x and a debt/equity ratio of 0.26, I believe the growth in debt is manageable, even though it is nearing a delicate situation with higher gearing.

More dilution to come

Acknowledging that the company lacks cash, the remaining $10 billion will be paid in shares, resulting in dilution to existing owners. With a market capitalization of $140 billion at the time of writing, this would imply a dilution of about 7%.

The silver lining is that Adobe will continue repurchasing shares in the foreseeable future (the company repurchased approximately 5.1 million shares during the recent quarter). At the present share price, 5.1 million shares are worth approximately $1.5 billion, which will assist in offsetting some of the dilutions, but not substantially.

(Potential) Positive Impact on Adobe’s bottom line in the short term

So, what are the upsides?

To give you an idea of their size and financial performance, Figma is forecast to add roughly $200 million in net new ARR this year, hitting $400 million in total ARR in 2022, with a net dollar retention rate of more than 150%.

With $400 million in revenue, Figma would contribute about 2 to 3% to Adobe’s annual revenue (about $17 billion TTM). To put things into perspective, the company is paying approximately 10% of its value for a 2 to 3% rise in revenue.

Is it worth it?

Ok, let us be more optimistic. Figma’s total addressable market is estimated to be roughly $16.5 billion by 2025 across design, whiteboarding, and collaboration according to Adobe’s presentation slides. Of course, Figma is unlikely to capture everything.

Let’s assume it can acquire roughly 30% of the market share, similar to Adobe, this would be around $4.95 billion. If this comes to fruition, Adobe’s annual income will climb by 29%. If this happens, then the agreement will be worthwhile in the long run.

But getting there is full of uncertainty. Adobe would require a compound annual growth rate of 130% over the next three years to reach $4.95 billion. Extremely ambitious.

The business also stated that the purchase would be accretive to Adobe’s earnings per share only after three years, so investors will have to wait. A wait that may provide higher returns but is highly risky, especially given how little we know about Figma’s financial health and outlook.

Concluding thoughts

There’s little doubt that this acquisition comes at a tremendous cost. It is evident from the dumping that most investors do not favour the deal. A few, however, would believe this is the best course of action because it widens its moat. In taking this risk, Adobe is betting that it can effectively integrate Figma with Adobe and that Figma can attain the addressable market it has projected for the company. In the next few years, Figma would either catapult Adobe to new heights or cause the business to suffer diminishing revenue.

That being said, what’s to say another firm doesn’t come in to compete with Adobe again? Will Adobe purchase the next competitor? How long could that be sustained?