The final earnings season of the year is wrapping up.

All three local banks have reported solid sets of earnings as their business is buoyed by the current high interest rate environment.

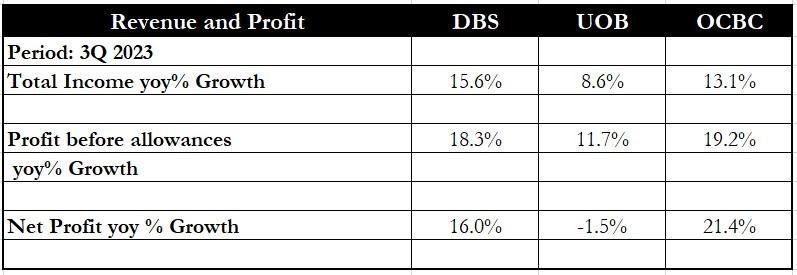

DBS Group (SGX: D05) reported a record total income of S$15.2 billion for the first nine months of 2023 (9M 2023) while United Overseas Bank (SGX: U11), or UOB, saw its total income for the same period jump 28% year on year to S$10.5 billion.

Not to be outdone, OCBC Ltd (SGX: O39) total income climbed 24% year on year for 9M 2023 to S$10.2 billion.

With these sets of robust results, investors may be wondering which bank offers the best value.

We look at different aspects of all three banks to try to determine this.

Financials

Starting with financials, we see that DBS reported the highest year-on-year increase in total income among the trio for the quarter.

Singapore’s largest bank enjoyed a 23% year-on-year rise in net interest income while fee and commission income also climbed by 9% year on year.

However, OCBC reported a slightly better year-on-year increase in profit before allowances of 19.2% versus DBS’s 18.3%.

Flowing through to the net profit line, OCBC saw the highest year-on-year increase with 21.4% with DBS coming in second at 16%.

Investors should note that both DBS and UOB reported a one-time expense relating to the integration of their respective purchases of Citigroup’s (NYSE: C) consumer banking business.

Excluding this one-off item, DBS’s net profit would have risen by 18% year on year while UOB’s net profit would have increased by 5% year on year instead of dipping.

Winner: OCBC

Loans and NIMs

Moving on to each bank’s loan book and net interest margin (NIM), we see that all three banks saw their loan numbers dip year on year.

The surge in interest rates could be responsible for the weak showing in loan growth.

However, all three banks made up for this with higher year-on-year NIMs.

OCBC’s NIM was the highest for 3Q 2023 at 2.27% but DBS saw the sharpest year-on-year NIM increase at 0.29 percentage points.

Both DBS and OCBC also enjoyed quarter-on-quarter growth in NIMs but UOB’s NIM fell by 0.03 percentage points from 2Q 2023.

OCBC is the winner in this category as its loan growth decline was less than DBS’s while its NIM was the highest among the three banks.

Winner: OCBC

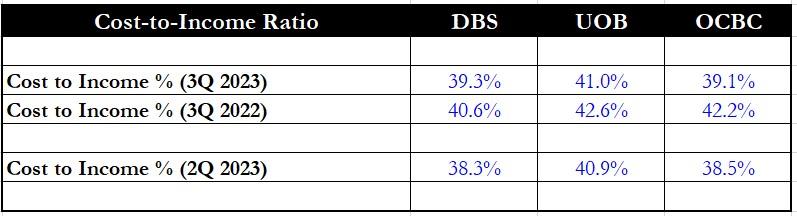

Cost-to-Income ratio (CIR)

Cost-to-income ratio, or CIR, is the next category we looked at.

The lower a bank’s CIR, the more efficient its operations.

OCBC has the lowest CIR for 3Q 2023, edging out DBS which won with the lowest CIR in the previous quarter (2Q 2023).

OCBC also saw the best improvement in its CIR with a 3.1 percentage point year-on-year reduction compared with DBS’s 1.3 percentage point year-on-year decline.

Winner: OCBC

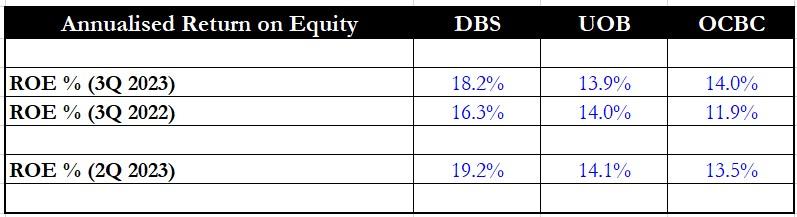

Return on equity (ROE)

Moving on to ROE, DBS is the hands-down winner with the highest ROE among the three for 3Q 2023.

It has also maintained this record in the previous quarter as well as in 3Q 2022.

Winner: DBS

Non-performing loans ratio (NPL ratio)

For the NPL ratio, OCBC boasts the lowest of the trio at 1% for 3Q 2023.

The lender saw a slight improvement over the 1.1% in 2Q 2023 and it was also a decline from the 1.2% reported a year ago.

DBS, however, saw its NPL ratio rise slightly as it had around S$100 million of exposure to Singapore’s landmark S$2.8 billion money laundering case and made provisions for this exposure accordingly.

Winner: OCBC

Valuation

Finally, we arrive at the valuation section where we determine which of the banks are the cheapest.

UOB wins in this case with a price-to-book (P/B) ratio of 1.1 times.

DBS is the most expensive of the trio with a P/B of 1.45 times while OCBC’s P/B stood at 1.14 times.

Winner: UOB

Get Smart: OCBC emerges the winner

In the previous quarter, both DBS and OCBC were tied with three winning factors each.

For 3Q 2023, the decision is clearer with OCBC emerging the winner by bagging four out of the six categories.

All three banks, however, sounded a cautious note as loan growth may remain tepid.

High interest rates are expected to persist which should continue to benefit the trio in 2024.

By the time your child grows up, inflation will have gobbled up their savings. If you not only want to protect their money but also grow it, there are 3 SGX stocks you can consider buying. One has already proven to give a 55.8% dividend pay rise. Get all the details in our latest special FREE report. Just click here.

Disclosure: Royston Yang owns shares of DBS Group.