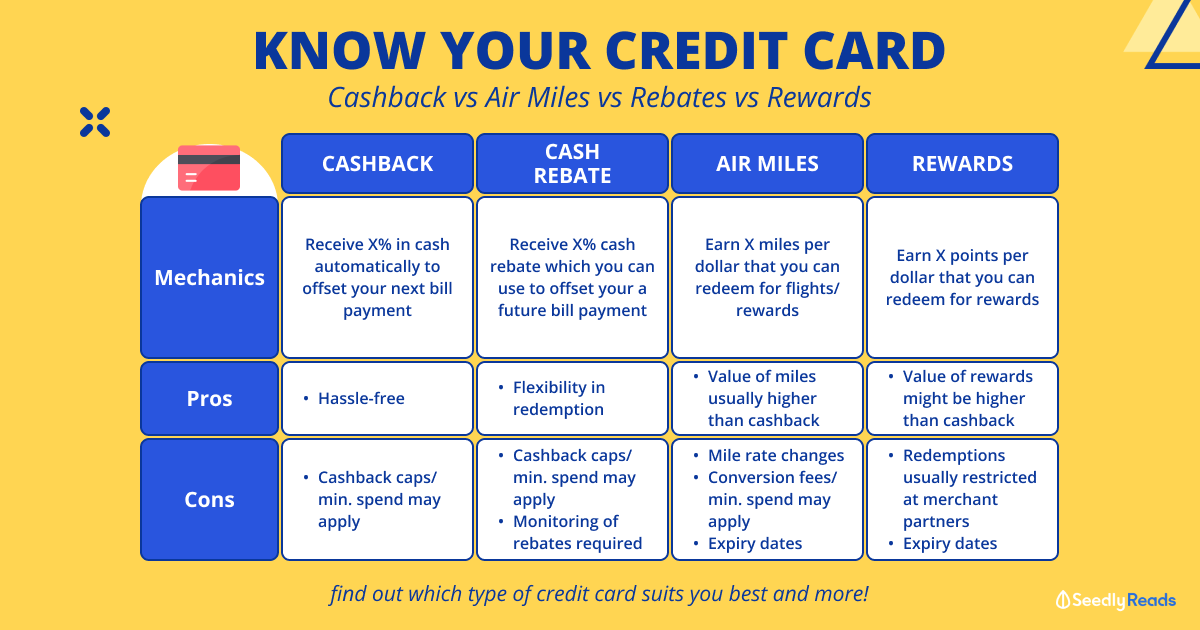

When deciding what’s the best credit card in Singapore to get.

You usually have to decide between earning credit card points, miles or cashback.

With points, you’ll often find that you need to accumulate something to the tune of 40,000 points (or $4,000 spent) just to get some eco-friendly reusable coffee cup.

And with miles, if you aren’t a frequent traveller or big spender, it’ll be hard to obtain that elusive first-class ticket.

Credit Cards With Cashback: Is Getting a Cashback Credit Card Worth It?

This… brings us to cashback credit cards, which basically give you ‘free’ money.

Let’s find out which is the best cashback credit card, shall we?

Disclaimer: The various credit cards all have their respective terms and conditions. So please read through them before deciding which credit card to get! Note that information is accurate as of 14 January 2024 and that promotions are subject to change without prior notice.

TL;DR: Best Cashback Credt Card in Singapore (2024): Which Credit Cards Give You More Cash Back?

These are the best cashback credit cards that you should be using:

| Cashback Credit Card | Cashback Rate | Total Monthly Cashback Cap | Min. Monthly Spend | Best For? |

| OCBC INFINITY Card Apply Now |

1.6% on virtually all spend (usual exclusions apply) |

No cap | $0 | Those looking for a reliable unlimited cashback card |

| Maybank Platinum Visa Apply Now |

3.33% on local and foreign currency spend | $66.67 $2,000 monthly spend |

$300 for three months | Those looking for a no-frills credit card with low min. spend and wide coverage |

| UOB EVOL Apply Now |

8% on Online spend 8% on Contactless spend 0.3% on Other spend |

$60 -$20 Online -$20 Contactless -$20 Other |

||

| Citi SMRT | 5% on online (exclude mobile wallet and travel-related transactions) 5% on groceries 5% on taxis, private-hire rides & SimplyGo public transport 0.3% base cashback for qualifying retail spend |

$600 annual cap | $500 |

Big-ticket items |

| UOB One Apply Now |

3.33% base cashback Up to 10% for bonus categories (existing cardholders) Up to 15% for bonus categories (new to UOB cardmembers) |

~$66.67 $200 per quarter |

$500 for 3 consecutive months |

|

|

Maybank Family & Friends |

8% on 5/10 selected categories 8% on all Malaysian Ringgit spend on top of 5 preferred categories |

$150 $25 for each bonus category |

$800 | Families |

If you’re wondering how I put together this list… I basically took advantage of countless work hours on research. So the next time you walk into a bank or any credit card roadshow, this will be you:

You’re welcome.

Click to Teleport

What Are Cash Back Credit Cards? Why Would The Banks Give Us Free Money?

The answer is in the fine print.

Most cash rewards programmes have a minimum spend requirement and a cashback cap.

So, while a card might offer you a generous 20% cashback.

You’ll probably need to spend around $10,000 a month to qualify.

And the maximum amount of cashback you can probably get is $50 a month.

Also. if you were wondering what cashback is, it often comes in the form of an offset of your credit card bill.

FOR EXAMPLE ONLY, PLEASE.

No such card exists.

However, most consumers do not take the time to read the fine print.

How Does Cashback Work? Which Bank Is Best for Cashback?

So, there is a chance that they might use a credit card under the impression that the cash rewards programme is more generous or applicable to a broader range of expenditures than they actually are.

And how many of us really track how much we spend to truly maximise our cashback rewards?

There are also plenty of consumers who might be under the impression that they can ‘afford to’ spend more because they’re getting cashback.

WRONG!

That’s awful news if you can’t make the payment on time.

The banks will charge high-interest rates (~28% p.a. that compounds daily) on credit, and the late fees for balances that are carried over are usually damn siao.

The lesson to take away here?

Only get a credit card if you are conscientious about your spending habits and can pay your credit card bills on time.

Please don’t chase credit card bonuses if you don’t need to spend on anything.

Back to top

What Are the Best Cash Rebate Credit Cards in Singapore (2024)?

To make your life easier, I decided to sort the various cashback credit cards into different categories that I think people would care about:

- No-frills credit card with low minimum spend, next to no exclusions and virtually no cashback cap.

- Daily expenses (Min. monthly spend of $600)

- Big-ticket items

- Groceries, Petrol, Food Delivery & more.

I’ve also listed the following:

- Cashback rate

- Monthly minimum spend

- Maximum cashback cap.

That’s not all.

As a value-added service, I’ve also included links to real user reviews left by our SeedlyCommunity to help you better decide which cashback credit card you should apply for.

Another essential thing to note is that there is no objectively best credit card.

The best credit card is the one that compliments your spending habits and allows you to maximise the cashback you can earn.

Back to top

Best Unlimited Cashback Credit Card

First up on the list we have no-frills, unlimited cashback credit cards. These cards have no minimum monthly spend requirement and no cap on cashback. Aside from the standard exclusions like payments made via AXS, educational institutions, e-wallet top-ups, payments to financial institutions, etc., these cards cover most categories.

1. OCBC Credit Cards: OCBC Infinity Cashback Card Review (2024)

The OCBC INFINITY Cashback Credit Card is a fuss-free unlimited cashback card that allows you to earn 1.6% cashback on both local and foreign currency spend.

Like other unlimited cashback cards, there is no minimum spend or cap. Also, the great thing about this card is that the cashback earned will be automatically credited to your OCBC INFINITY card account.

OCBC Infinity Card Basics

- Cashback:

- 1.60% on local and foreign currency spend

- Min. Monthly Spend: $0

- Cashback Cap: N.A.

- Annual Fee: $196.20

- Spend $10,000 in one year, starting from the month after your OCBC INFINITY Cashback Card was issued to get your annual service fee automatically waived

- Effective Interest Rate: 27.78% p.a.

- Income Requirement:

- $30,000 for Singapore Citizens or SPRs

- $45,000 for foreigners

- Minimum Age: 21

OCBC INFINITY Cashback Card Promotion

If you are a new to OCBC Cardmember, be the first 2,000 whose OCBC INFINITY Cashback Card is approved each month to earn a bonus of 0.2% cashback for the first $3,000 qualifying spend charged to your new card monthly for six months from the card approval date. This is on top of your existing 1.6% in unlimited cashback for 1.80% in cashback in total. The promotion ends on 31 March 2024. T&Cs apply.

Apply Now

Additional Considerations

The OCBC INFINITY credit card is an unlimited cashback credit card, which means that you can get 1.6% cashback on virtually ALL your spending with no minimum spending or caps!

But wait a minute, other cards give higher cashback, right? Like the UOB Absolute Cashback (1.7%), American Express True Cashback (3.0% for the first 6 months on $5,000 spent and 1.5% thereafter) or the Citi Cash Back Plus (1.60%).

Let me explain! For any American Express card, which the UOB Absolute is too, you might find it hard to find merchants where you can use the card due to the lack of acceptance. Otherwise, AMEX cards would easily be number one.

As for the Citi Cash Back Plus, cashback can only be redeemed via SMS, which is an extra hurdle for just 0.10% cashback.

The OCBC INFINITY credit card, on the other hand, is a MasterCard that is widely accepted and automatically offsets your next credit card bill with the cashback you’ve earned, hence making it the number one fuss-free credit card for all your spending needs.

The cashback rate is a little low, but then again, you really can’t put a price tag on simplicity!

Honourable Mention: Standard Chartered Credit Cards — Simply Cash Credit Card

But, If you have a Standard Chartered savings account and do not want to go all in on the OCBC ecosystem.

Another no-frills card to consider is the Standard Chartered Simply Cash Credit Card:

Standard Chartered Simply Cash Credit Card Basics

- Cashback:

- 1.5% on virtually ALL spend (Except the usual credit card exclusions such as insurance payments and top-ups to wallets)

- Min. Monthly Spend: N.A.

- Cashback Cap: N.A.

- Annual Fee: $196.20 (first year waived)

- Effective Interest Rate: 27.90% p.a.

- Income Requirement:

- $30,000 per year for Singaporeans and PRs

- $60,000 for Foreigners

- Minimum Age: 21

Back to top

Best Credit Cards With Low Minimum Spend: UOB Absolute Cashback Card and AMEX True Cashback?

If you want to spend a bit more, here is a straightforward credit card with a low minimum spend requirement and almost no exclusions.

The choice is clear as, unfortunately, 2022’s pick, a combination of the AMEX True Cashback Card (1.5% cashback) or the UOB Absolute Cashback Card (1.7% cashback) with the GrabPay Mastercard has been nerfed to oblivion.

But all is not lost. You can still get a cashback card with 3.33% cashback, which is not too bad.

Back to top

Enter the Maybank Platinum Visa credit card.

Maybank Platinum Visa Basics:

- Cashback:

- 3.33% on local and foreign currency spend

- 3.33% on insurance payments, but do note that insurance payments can be accumulated as eligible spending for only half of the monthly spending amount for each tier

- Min. Monthly Spend: $300 | $1,000 | $2,000

- Cashback Cap: $30 | $100 | $200

- Annual Fee: No annual credit card fee

- A quarterly service fee of $20 is waived under the three-year fee waiver. Subsequently, the quarterly service fee is waived when you charge to your Card once every three months

- Effective Interest Rate: 27.90% p.a.

- Income Requirement:

- $30,000 for Singapore Citizens or Singapore Permanent Residents (SPR)

- $45,000 for Malaysia Citizens in employment for at least 1 year

- $60,000 for other nationalities, in employment for at least 1 year

- Minimum Age: 21

The Maybank Platinum Visa Card stands out as the top choice for individuals who don’t spend much due to its low monthly spending requirement of $300. Cardholders can enjoy a generous 3.33% cashback, capped at $200 per quarter:

|

Tier |

Min. monthly spend in the quarter |

Maximum cashback |

||

| July | August | September | ||

| 1 | $300 | $300 | $300 | $30 |

| 2 | $1,000 | $1,000 | $1,000 | $100 |

| 3 | $2,000 | $2,000 | $2,000 | $200 |

| The above table is for illustrative purposes only. | ||||

Moreover, cardholders receive valuable perks such as complimentary travel insurance. What’s even better is that the $20 quarterly service fee is waived for the first three years after signing up. Subsequently, this fee is automatically waived simply by using the card once every three months, making the Maybank Platinum Visa Card a hassle-free way for budget-conscious individuals to maximize their cashback benefits.

But, a quirk with Maybank is unlike other credit cards; Maybank’s billing cycles are based on the calendar month and not the statement month. So, your billing cycles will be from the days of the month and not your billing cycle. For example, for January, the minimum monthly spend must be made between 1 -31 January 2024.

Apply Now

Back to top

Highest Cashback Credit Cards for Daily Expenses

However, if you spend more than $600 a month on your credit card, you can earn a bit more cashback with either the UOB EVOL Card:

3. UOB Credit Cards: UOB EVOL Review (2024)

You might be wondering about the OCBC Frank card, which was included in 2022.

Unfortunately, it was nerfed pretty heavily. Before November 2022, online and contactless spending had separate cashback caps of $25 each.

Now, online and contactless spending share the same $25 cap, which, frankly, is a bit mediocre.

Like the OCBC Frank card, the DBS LiveFresh card was nerfed, too, but more on that later.

This is why I am considering only the UOB Evol Card for this article:

| Cashback Credit Card | UOB EVOL |

| Total Cashback Cap Per Month | $60 |

| Monthly Minimum Spend | $600 |

| Cashback (Online Spend) & Monthly Cap |

8% |

| Mobile Contactless Spend (Via Apple Pay, Google Pay, Samsung Pay or Fitbit Pay) & Monthly Cap |

8% |

| Contactless Spend (Includes PayWave + Mobile Apps) & Monthly Cap |

— |

| Green Cashback (Selected Eco-Eateries, Retailers and Transport Services) | — |

| Other Spend | 0.3% ($20) |

| Annual Income Requirement |

$30,000 (Singaporeans / PR) |

| Annual Fee |

$196.20 |

| Interest Rate | 27.80% p.a. |

| Application Link | Apply Now |

Realistically, we would start with the assumption that you make an effort to split your credit spend between contactless and online spending equally and ignore the ‘any other spend’ category as it is hard to hit.

The UOB EVOL card is the winner with its high 8% cashback rate.

However, upon close examination, you cannot hit an effective cashback rate of 8% as you are limited by the monthly cashback caps for online and contactless spend categories, which add up to $40 per month ($20 per category). This means you only get cashback for $500 spent each month.

Let’s say you look at your monthly statement and realise you spend only about $600 per month. Your effective cashback rate is still 6.67% ($40/$600), which is pretty decent but not 8% as advertised.

If you spend more than ~$667 per month, your effective cashback rate drops to 5.99% ($40/$667).

But another essential thing to note is that you do not get cashback with UOB EVOL for any transactions at UOB$ merchants where UOB$ are issued (previously known as SMART$).

Instead, you will get UOB$ cashback:

- Up to 10% cashback: Get UOB$ cashback on all in-store purchases at participating outlets

- Automatically offset your spending: Use your earned UOB$ on your next bill at the same merchant.

UOB$ Merchants

Speaking of merchants, here is a list of UOB$ merchants:

| Category | Merchants |

| Food and Beverage | BreadTalk Toast Box Yole Sushiro A&A Bistro & Café Hei Sushi Kinara North West Little Italy MOA Restrobar Sakae Sushi Smooy Tenkaichi Japanese BBQ Restaurant OSO Ristorante Kinara Contemporary Indian Cuisine Mr Briyani Orchid Live Seafood Bonchon Carl’s Jr Taste of India Aburi-EN Baker & Cook Bee Cheng Hiang Canteen by Trapeze Rec. Club Cellarbration Co Chung Crystal Jade Group 8 Degrees Taiwanese Bistro Famous Kitchen Famous Palace Famous Treasure Feng Tian Xiao Chu Francesca’s Hard Rock Cafe I.N.U Cafe and Boutique Mr. Coconut Mun Zuk Nanbantei Japanese Restaurant PastaGo Patisserie G Polar Puffs and Cakes Potato Corner Starbucks Tangmen Restaurant Tian Tian You Yu Yuan Cuisine Group |

| Gourmet Dining | Kappou Miyako Bincho Hortus Kotuwa Meatsmith Little India Meatsmith Telok Ayer Restaurant Majestic The Market Grill & Wine 90 |

| Groceries | Cold Storage Giant Jason’s Deli |

| Retail and Services | Hall of Fame LFC Aesthetic Works MediSpa CASA COSLAB The Stretch Clinic agnès Ba Buf’d Nail Spa Crocodile Delta Dental Surgeons Gordon Max G-Star Raw Guardian Hang Ten HoneyWorld iRUN Le Coq Sportif Limited Edit Underground Maco Nail Spa Miniso M)phosis Mr Jeff New Era Nitori nOptique Paris Miki Picota Nail Spa Pixie Nail Spa Qoosh Nail Spa Replay Salivan Beauty Clinic Sports Fashion Surfer’s Paradise Winter Time Western Corp |

| Travel and Entertainment | Cathay Cineplexes City Tours |

Source: UOB

This situation is not ideal as although some merchants do offer 10% cashback, you are stuck with 1% cashback at Cold Storage and Giant, which is way lower than UOB EVOL’s cashback rate of 6.67%.

Not to mention that you will have to use it back at the same merchant.

Alternatively, you can look at the DBS Live Fresh card, where you will not exceed the cashback cap by hitting the minimum spend if you split your credit spend between contactless and online spending equally.

Bonus: DBS LiveFresh Review (2024) — Nerfs and a Silver Lining

On 1 February 2024, DBS announced the following changes to the DBS Live Fresh card, which take effect from 1 March 2024:

- Cardmembers will earn unlimited 0.3% base cashback on all eligible spend.

- Upon hitting the minimum spend requirement of $800 per calendar month, Cardmembers will enjoy up to 6% cashback on Shopping and Transport spend (includes instore, contactless and online transactions made in Singapore and overseas):

- 6% cashback (0.3% + 5.7% bonus) cashback on Shopping spend (capped at $50 per calendar month and ~$877.20 monthly spend)

- 6% cashback (0.3% + 5.7% bonus) on Transport spend (capped at $20 per calendar month and $333.33 monthly spend)

- The card benefits of up to 5% cashback on Contactless and Online Spend, and the extra 5% Green Cashback on Sustainable Spend will cease.

The DBS LiveFresh credit card has undergone some adjustments. The minimum monthly spend requirement has been raised from $600 to $800 to qualify for higher cashback. Additionally, the range of transactions eligible for increased cashback has been restricted to shopping and transportation, excluding dining and groceries. Furthermore, the extra 5% Green Cashback has been removed.

However, there are positive changes too. The cashback rate has been bumped to 6%, and the shopping category now has a higher cashback cap ($877.20) than the monthly spend requirement of $800. So, even though it’s tougher to meet the spending target, you can still earn more cashback if you spend over $800, especially on. bigger purchases.

There is a silver lining.

DBS LiveFresh card could become more advantageous in certain spending scenarios. While it may lose its status as a primary card for many users, particularly in comparison to alternatives like the UOB EVOL card, it could become a valuable card for cerertain purchases, offering competitive cashback rates for transactions exceeding the new spend requirement.

Back to top

Best Credit Cards for Big Purchases

Planning a wedding?

Need to renovate your brand-new BTO?

Planning to get a laptop?

Check out these cards to save BIG.

4. Citibank Credit Cards: Citi SMRT Card Review 2024

For any big-ticket online purchases, you’ll want to get the Citi SMRT Credit Card.

Citi SMRT Card Basics

- Cashback:

- 5% cashback on online purchases (excludes mobile wallet and travel-related transactions) | Supermarkets & grocery stores | Taxis and private hire rides & SimplyGo transactions for public transport

- 0.3% savings on all other qualifying retail spend

- No monthly cap on how much SMRT$ you can earn

- Min. Monthly Spend: $500

- Cashback Cap: No monthly cap on how much SMRT$ you can earn but an annual cap of 600 SMRT$ earned, i.e. $12,000 spent in 12 months (Every 1 SMRT$ shall, unless otherwise specified, represent $1 in cash value)

- Annual Fee: $196.20 (Waived for the first two years)

- Effective Interest Rate: 27.90% p.a.

- Income Requirement:

- $30,000 per year for Singaporeans / PRs

- $42,000 for foreigners

- Minimum Age: 21

Citi SMRT Card Cashback

With this card, you’ll get a pretty decent 5% cashback rate on the following spend categories:

- All supermarkets and grocery stores

- Taxi and public transport rides (including private-hire rides)

- Online purchases

But do note that bonus cashback will not include online purchases as follows:

- Mobile Wallet purchases from merchants like IPAYMY, CARDUP, YOUTRIP, EZ-LINK and EZL AUTO TOPUP

- Travel-related transactions include but are not limited to transactions that bear the following MCCs:

- MCC 3000 to 3350 Airlines, Air Carriers

- MCC 3351 to 3500 Car Rental Agencies

- MCC 3501 to 3999 Lodging – Hotels, Motels, Resorts

- MCC 4112 Passenger Railways

- MCC 4411 Cruise Lines

- MCC 4511 Airlines, Air Carriers (Not Elsewhere Classified)

- MCC 4722 Travel Agencies and Tour Operators

- MCC 5962 Direct Marketing – Travel-Related Arrangement Services

- MCC 7011 Lodging – Hotels, Motels, Resorts (Not Elsewhere Classified)

- MCC 7512 Car Rental Agencies (Not Elsewhere Classified).

Citi SMRT Card Monthly Minimum Spend and Cashback Cap

But note that you must spend at least $500 monthly to unlock this 5% cashback rate (SMRT$).

Note that redemption of SMRT$ for shopping vouchers and cash rebates has to be performed online or via SMS in blocks like this:

| Cash rebate redemption amount | SMRT$ required | SMS keyword |

| $10 | 10 | SMRT10 |

| $50 | 50 | SMRT50 |

| $100 | 100 | SMRT100 |

This means that you will have to have at least $10 worth of SMART$ before you can redeem any rebate.

If your total monthly statement of retail purchases falls below $500, the eligible rebate rates will be reduced to 0.3%.

The beauty of this card for big-ticket online purchases lies in how Citi arranges the cashback cap. Remember to use the card directly to pay for your stuff, as the card does not support mobile wallets. This card should not be used for travel transactions.

Unlike most cards with a monthly cashback cap, the Citi SMRT card has an annual cashback cap of $600.

This means that at any point within 12 months, you can spend up to $12,000 and get 5% or up to $600 cashback on eligible spending.

Note that the annual cashback cap resets every 12 months. So you might want to apply for the card now, as the earlier you apply, the faster it refreshes the cap.

For example, if you only need to buy your big ticket nine months later, you can fully utilise the $12,000 cap within 3 months till the cap is refreshed.

Back to top

5. UOB Credit Cards: UOB One Card Review (2024)

The Citi SMRT card may be suitable for online transactions, but there’s a gap for in-store transactions.

That’s where the UOB One Card comes in.

Apply Now

UOB One Basics

- Cashback:

- Base 3.33% cashback on all retail spend [$500, $1,000 or $2,000 per month (min. five purchases a month) consecutively for three months]

- Up to 10% cashback for spending on bonus categories for existing UOB credit cardmembers

- Min. Monthly Spend for one Quarter: $500 | $1,000 | $2,000

- Cashback Cap:

- $50, $100 or $200, respectively, per quarter for base cashback

- Additional cashback capped at $100 a month

- Annual Fee: $196.20

- Effective Interest Rate: 27.80% p.a.

- Income Requirement:

- $30,000 per year for Singaporeans

- $40,000 for Foreigners

- Able to provide a fixed deposit collateral of at least $10,000 if you don’t meet the above income requirement

- Minimum Age: 21

If you are planning to make big purchases in the coming months and are willing to do a bit of planning, you can consider the UOB One Card.

P.S. It is possible to split bill payments between credit cards at some physical stores.

This is because the card offers a relatively high cashback rate of up to 3.33% on almost all purchases with a minimum spend of $500 / $1,000 / $2,000 per month and a minimum of five transactions per statement month for a qualifying quarter.

To qualify for this cashback, you must also spend $500 / $1,000 / $2,000 per month for three consecutive months.

But keep in mind that this is a flat rate and that the minimum spending requirements are relatively high.

Bonus UOB One Cashback: Shopee Cashback Singapore, Dairy Farm Cashback and More

In addition to the quarterly rebate, you will stand to receive additional cashback from these categories:

Cardmembers who have been awarded the $100 or $50 quarterly cashback for spending $1,000 or $500 a month for three months will get an additional 5.0% cashback. Whereas cardmembers who have been awarded $200 quarterly cashback for spending $2,000 for three months. Both categories will get an additional 6.67% cashback from these merchants:

- McDonald’s

- Dairy Farm Retail Group such as Cold Storage, CS Fresh, Giant, Guardian, 7-Eleven, Marketplace, Jasons, Jasons Deli,

- Grab (excludes mobile wallet top-ups)

- Shopee Singapore transactions (excludes ShopeePay), SimplyGo (bus and train rides)

- UOB Travel (excludes online and flight-only bookings)

Also, all Cardmembers who have been awarded the quarterly cashback will get an additional 1% cashback on Singapore Power utilities bill (excluding payments via AXS) successfully charged and posted to the Card Account in each statement month. They will also get an additional 1.67% cashback on Shell transactions successfully charged and posted to the Card Account in each statement month.

Do note that all additional cashback will be capped at $100 per month.

Here’s an example of how this works:

For the example above, the person qualified for the quarterly tier rebate as they spent precisely $500 each month for the whole quarter (three months) and got $72 cashback.

In addition, the person also spent on these additional categories and got $22 more on top of the base cashback of $50 for $72 cashback for the quarter in total.

Back to top

UOB One Credit Card Promotion

Get enhanced cashback of up to 15% cashback on McDonald’sNEW, DFI Retail Group, Grab, Shopee, SimplyGo (bus and train rides) and UOB Travel transactions when you apply for a UOB One Credit card till 31 Mar 2024.

Back to top

Best Cashback Credit Card For Families

Everybody must visit the supermarket to get stuff like milk, diapers, bananas, soy sauce, and bread… You get the picture.

Even driving out will cost petrol, which costs money. And for days that you are too tired to cook, you might order food delivery occasionally.

Why not save a bit while making these necessary purchases with the Maybank Family and Friends Card:

6. Maybank Credit Cards: Maybank Family and Friends Card Review (2024)

Apply Now

Maybank Family and Friends Card Basics

- Cashback:

- 8% on five out of 10 selected categories

- Minimum Monthly Spend: $800

- Cashback Cap: $125 ($25 for each bonus category)

- Annual Fee: $180 (first three years waived)

- Effective Interest Rate: 26.90% p.a.

- Income Requirement:

- $30,000 per year for Singaporeans or SPR

- $45,000 for Malaysians in employment for at least 1 year

- $60,000 for Foreigners in employment for at least 1 year

- Minimum Age: 21

Maybank Family and Friends Cards Categories

With this card, you can earn 8% cashback globally on five out of these 10 cashback categories:

| Eligible Categories For Local, Overseas and Online Spend |

Description |

|---|---|

| Groceries | NTUC FairPrice/Finest/X‐tra, Cold Storage, Giant, Market Place, Jasons, Sheng Siong, DON DON DONKI, HAO Mart, RedMart, Amazon Fresh and all other grocery stores and supermarkets globally |

| Dining & Food Delivery | Restaurant dining, Foodpanda and Deliveroo globally |

| Transport | Petrol stations, Contactless bus and train rides, Limousines, Taxi, Grab/GOJEK rides, other passenger transportation services and automotive-related services globally |

| Data Communication & Online TV Streaming | StarHub, Singtel, M1 Limited, Circles.Life, MyRepublic, Disney+, Netflix and/or other telecommunication, pay television, cable and radio services globally. |

| Retail & Pets | POPULAR Bookstores, Toys ‘R’ Us and Yamaha Music, pets and veterinary related services globally |

| Online Fashion | Online purchases on Apparels, Shoes, Accessories, Leather goods, Luggage and other fashion purchases globally |

| Entertainment | Bars, Drinking places, Cinemas, Motion Picture Theatres, Theatrical Producers and Ticketing agencies globally |

| Pharmacy | Guardian, Watsons, Unity, GNC/LAC, other drug stores and pharmacies globally |

| Sports & Sports Apparels | Sports/Riding apparels, Sporting goods, Bicycle shops, Recreation & sporting camps, Athletic fields, Commercial sports, Professional sport club, Golf courses, Country clubs and Membership (Athletic/Recreation/Sports) globally |

| Beauty & Wellness | Massage parlors, Health & beauty spas and Barber shops globally |

FYI: Selected Categories will take effect on the first day of the following calendar month. The Selected Categories will apply to the Cardmember for three months from the effective date (“Lock-In Period”). Maybank reserves the right to amend the length of the Lock-In Period from time to time without prior notice or liability to any person.

To get the 8% cash rebates, cardholders must spend a minimum of $800 per calendar month.

Any monthly spending from $0 – $799 will only receive 0.3% in cashback.

Also, after reaching the monthly cashback cap for a selected category, the 0.3% cashback will be applied to further spending that month and the 0.3% cashback applies to all other spend on non-selected categories.

There is also a total cashback cap of $125 ($25 for each category).

Bonus Category for Maybank Family and Friends: Additional 8% cashback on Malaysian Ringgit Spend

Those who love going to Johor Bahru for a weekend getaway can now earn an additional 8% cashback on top of your five preferred categories!

After reaching your monthly cashback cap, the 8% cashback will be applied to the Malaysian Ringgit for the selected category spending that month and all other Malaysian Ringgit spend on non-selected categories in the month:

| Min. monthly spend | Cashback on five selected categories | Cashback on Malaysian Ringgit on other spends (above and/or outside of selected categories) |

| $800 | 8%

(Up to $125 in total per calendar month, capped at $25 per category) |

8% (Additional cap of $25) |

| $0 – $799 | 0.3% | 0.3% |

More specifically, according to the card’s terms and conditions, the Malaysian Ringgit bonus category and cap applies to:

- Eligible retail transactions charged in Malaysian Ringgit on his/her Card that are not transactions which fall under Cardmember’s Default Categories or Selected Categories (as the case may be); OR

- Eligible retail transactions charged in Malaysian Ringgit on his/her Card which also fall under one of the Cardmember’s Default Categories or Selected Categories (as the case may be) after the Cardmember has charged more than $312.50 to that Default Category or Selected Category (as the case may be) during that calendar month.

However, note that Malaysian Ringgit transactions will incur a 3.25% foreign transaction fee. But, the 8% cashback if you hit the minimum spend of $800 more than covers it.

Back to top

So… Which Credit Card is the Best Benefit for You?

Have a favourite cashback credit card?

Believe that you’ve found a way to game the cashback credit card system to get the most amount of cashback?

Share with the community on Seedly lah…

Related Articles: